If you work in Indian fintech, you have heard the phrase “India Stack” more times than you can count. It appears in pitch decks, investor memos, and government press releases with remarkable frequency. But most explanations of it are either too technical or too vague to be useful.

Here is a plain-language explanation of what India Stack WealthTech actually means — what the infrastructure is, why it matters specifically for wealth management, and why building natively on it is the single most important architectural decision any India Stack WealthTech startup can make.

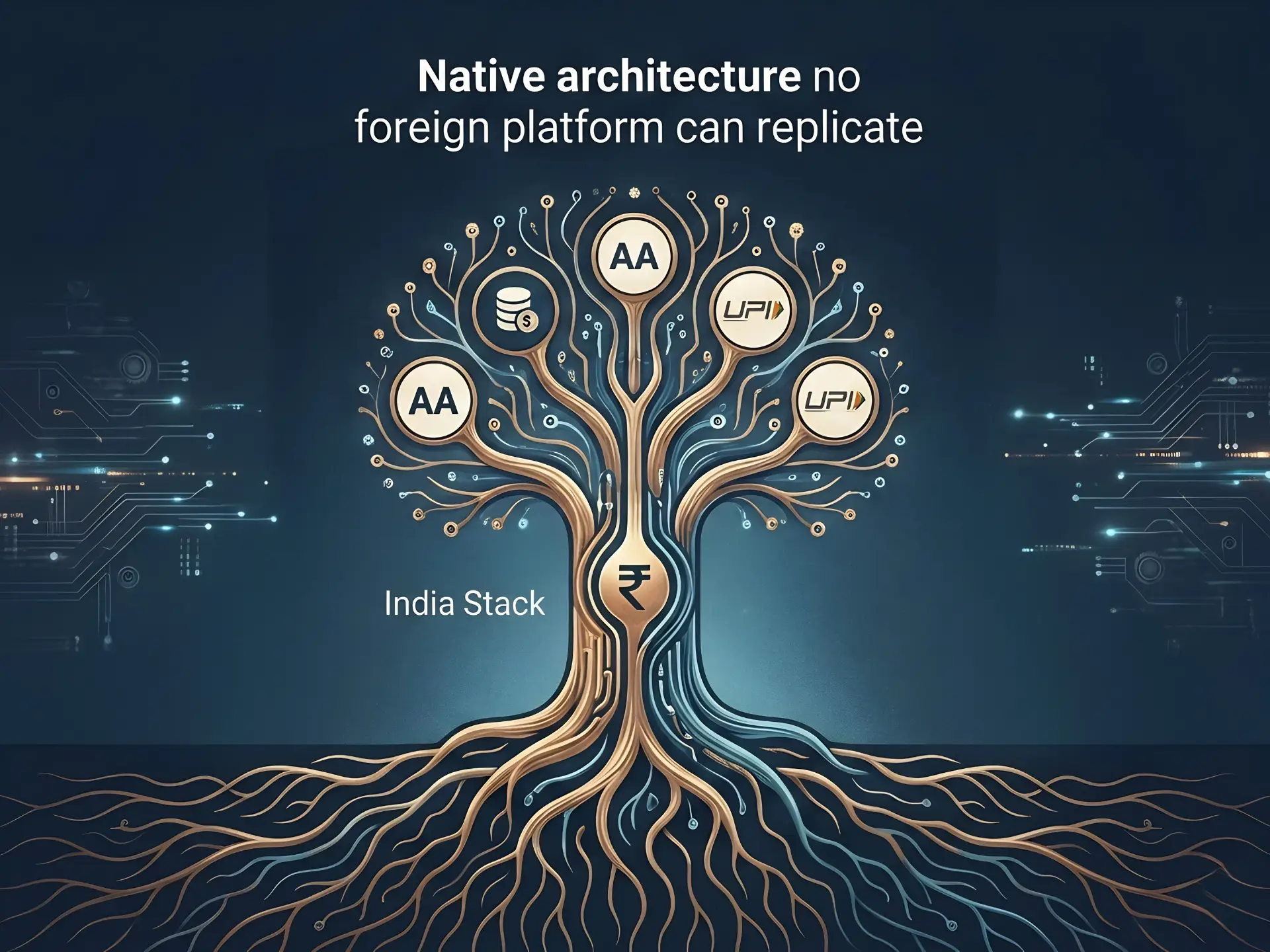

“India Stack is not a single product. It is a layered set of open digital infrastructure that any regulated entity can build on — and that no foreign platform can replicate from the outside. That is the competitive moat every India Stack WealthTech platform inherits from day one.”

India Stack is not a single API. It is a layered set of open digital infrastructure that any regulated entity can build on — and that no foreign platform can fully replicate from the outside.

The distinction matters because there is a meaningful difference between integrating India Stack and building on India Stack. Integrating means you built your product for a different context and added Account Aggregator or UPI as features. Building natively means your product would not make sense without these rails.

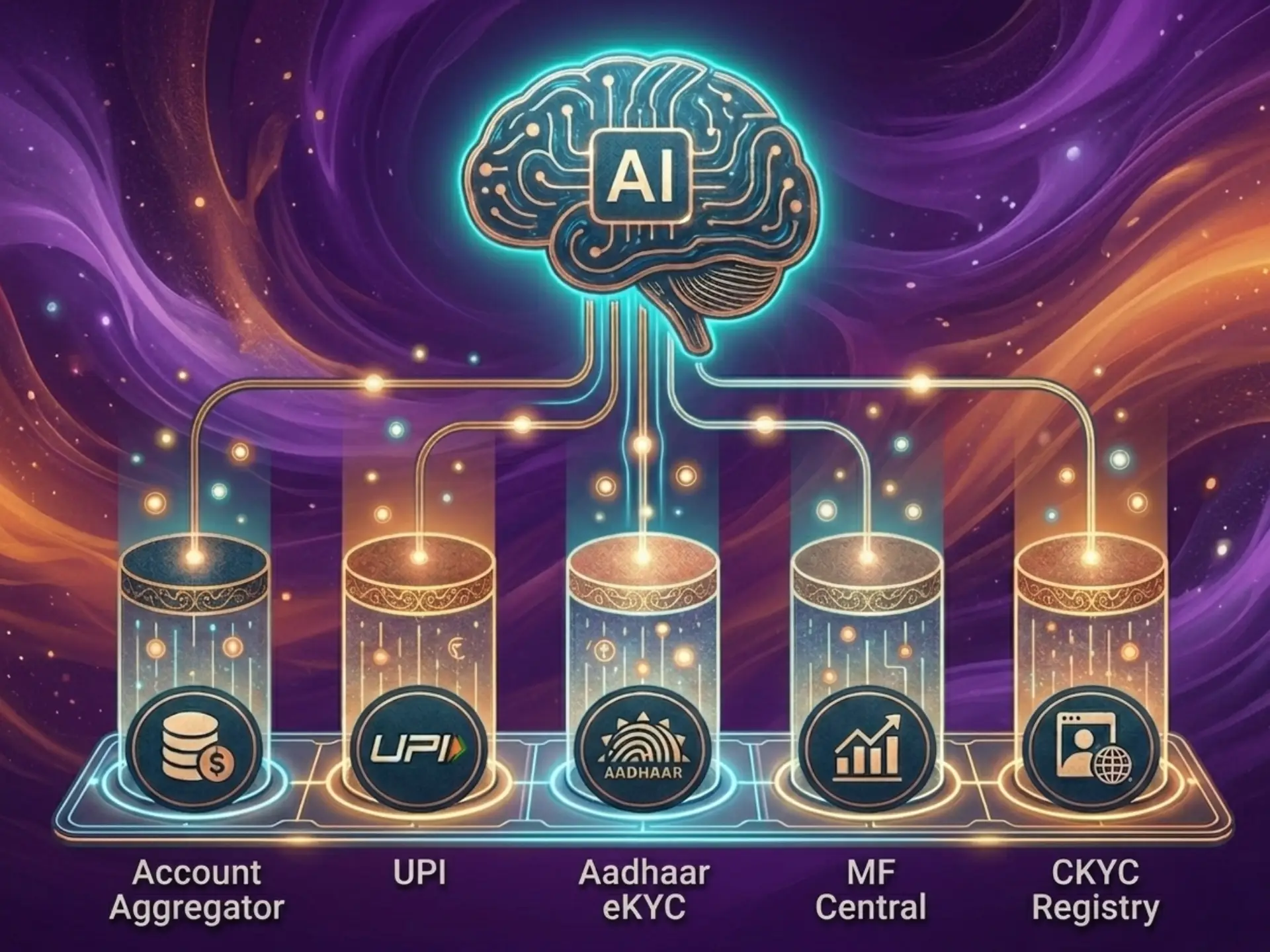

The 5 India Stack rails every WealthTech startup needs

India Stack is the collective name for a set of open digital infrastructure layers built and maintained by the Indian government and associated bodies. For WealthTech specifically, five rails are transformative:

Account Aggregator (AA) — A consent-based data sharing framework regulated by RBI. A user can share their complete financial picture — all bank accounts, all investments, all loans, all insurance — with a regulated platform in under 60 seconds. No passwords shared. No screen scraping. Clean, consented, auditable data. This is the most transformative rail for India Stack WealthTech.

UPI — Unified Payments Interface. ₹20 lakh crore in monthly transactions. The payment rail that eliminated friction in moving money. For WealthTech, it means seamless investment flows, instant redemptions, and frictionless onboarding payments.

Aadhaar eKYC — Paperless identity verification. Reduces customer onboarding from days to minutes. A user can verify their identity and complete KYC in under two minutes using Aadhaar OTP or biometrics.

MF Central — A consolidated mutual fund data platform. Complete holdings, transaction history, and NAV data across all fund houses in one place. For an AI model giving wealth guidance, this is the data layer that makes fund-level recommendations possible.

CKYC Registry — Central KYC records shared across financial institutions. A user who has completed KYC with one institution does not need to repeat it with another. Dramatically reduces onboarding friction for new WealthTech platforms.

Account Aggregator enables a user to share their complete financial life — bank accounts, investments, insurance, pension — with a regulated platform in under 60 seconds, with full consent and full control.

Why Account Aggregator changes everything

Before Account Aggregator, getting a comprehensive picture of someone’s financial life required either asking them to fill in long forms — incomplete, inaccurate, and frustrating — or screen-scraping their net banking portals, which is insecure, unreliable, and legally grey.

Neither approach gave you data quality good enough to build genuine AI guidance on top of. And without quality data, AI recommendations are generic at best and misleading at worst.

With Account Aggregator, an AI model can see your salary account transactions, your existing SIP portfolio, your outstanding home loan, your term insurance, and your EPF balance — all at once, all verified, all consented. That complete picture is what makes personalised AI guidance possible.

The consent architecture is also important. When you share data through Account Aggregator, you specify which accounts to share, what type of data, for how long, and for what purpose. You can revoke at any time. The Account Aggregator maintains an immutable audit log of every sharing event. This is not just good for users — it is legally clean data for the platform receiving it.

Native vs integrated — why the difference is a competitive moat

Most established WealthTech platforms were built before Account Aggregator existed. Their data models, user journeys, and product logic were designed around forms, screen scraping, or manual entry. Account Aggregator was added later — as a feature, not as a foundation.

The result is an integration seam. The product works, but the AI cannot reason across the full data picture because the architecture was not designed for it. Recommendations are bounded by what the original product was built to know.

Nivyo.AI is built the other way around. Account Aggregator is not a feature we added. It is the data foundation the entire product is built on. Every user journey starts with Account Aggregator consent. Every AI recommendation is made against Account Aggregator data. The product would not make sense without it.

This is what India Stack WealthTech built natively looks like — and it is a competitive moat that no foreign platform integrating from the outside can replicate at the same depth.

Building natively on India Stack means the data architecture, user journeys, and AI reasoning engine are all designed around these rails — not adapted to work with them after the fact.

What this means for Indian investors

For the average Indian investor, India Stack WealthTech means something simple and important: you no longer have to explain your financial situation from scratch every time you use a new platform.

You give consent once. The platform sees what it needs to see — your complete financial picture. It gives you useful, specific guidance based on your actual situation, not generic advice. And you maintain full control — you can revoke consent at any time, and the platform’s access ends immediately.

That is the experience Nivyo.AI is built to deliver. And the five India Stack rails above are the infrastructure that makes it possible — available to any regulated Indian platform, replicable by no foreign competitor.

This is what every India Stack WealthTech startup should be building — and what Nivyo.AI delivers.